Implementing Performance Systems in Tax Administrations with ITAS

Integrated Tax Administration Systems (ITAS) form the backbone of modern tax agencies, enabling streamlined processes like registration, assessment, returns processing, payments, audits, and collections. These systems support performance measurement by providing real-time data across core modules, allowing tax administrations to track key indicators organization-wide. A robust performance system leverages ITAS data to define measurable ranges, assign points, and aggregate scores up the hierarchy for fair evaluations.12

Understanding ITAS Foundations

ITAS integrates core tax processes into a unified platform, including taxpayer registration, accounting, refunds, verification, appeals, and enforced collection. This integration promotes end-to-end planning, better taxpayer experiences, and reliable data for oversight, ultimately boosting compliance and revenues. Existing ITAS components like reporting, analytics, case management, and risk tools already capture operational metrics, minimizing the need for new builds.1

In practice, ITAS modules generate data on filing compliance, payment timeliness, audit outcomes, and refund processing speeds. Tax administrations can use these without major customizations, as commercial products like SIGTAS or TRIPS include built-in performance reporting. This leverages “existing information” by querying databases for standardized KPIs such as registration accuracy, returns processed, or debt recovery rates.21

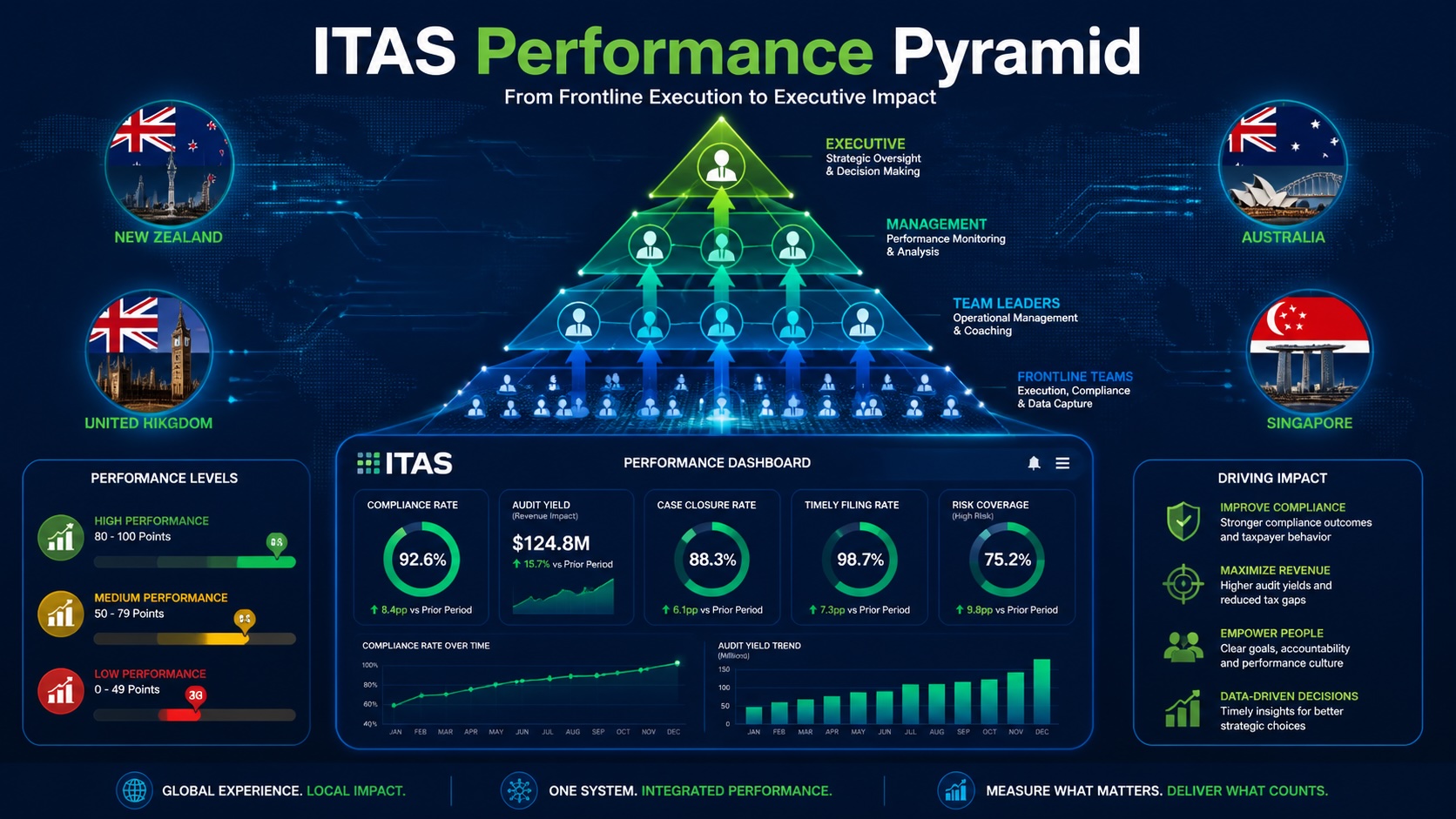

Designing Range-Based Performance Scoring

A points-based system standardizes evaluations by defining performance ranges for KPIs and assigning scores that roll up hierarchically. For instance, categorize metrics into ranges like low (0-30 points), medium (31-70), and high (71-100), based on targets derived from historical ITAS data. This allows team leads to sum individual scores into departmental totals, and directors to aggregate further, ensuring objectivity across structures.342

Key steps include selecting ITAS-sourced KPIs: voluntary compliance rates, audit yields, taxpayer service response times, and collection efficiency. Assign points proportionally; for example, a filing compliance rate of 90-100% earns full points, scaling down linearly. Aggregation uses weighted averages, with frontline staff (50% weight) feeding into mid-level (30%) and executive (20%) scores, promoting alignment.4562

Establishing Balanced Range Values

Ranges must avoid extremes: not too ambitious, risking universal failure, nor too lenient, inflating top performers. Base thresholds on benchmarks from prior years’ ITAS data, aiming for 20-30% in top brackets, 40-50% medium, and 20-30% low to reflect realistic distributions. Analyze historical variances; if average audit closure is 60 days, set ranges at <45 (high), 45-75 (medium), >75 (low).572

Pilot testing refines values: run simulations on 12-24 months of ITAS logs to ensure 25% achieve high scores without gaming. Adjust annually using statistical methods like quartiles from agency-wide data, preventing demotivation or complacency. This data-driven calibration, common in public sector adaptations of Balanced Scorecard, maintains credibility.894

ITAS Integration Mechanics

Embed scoring in ITAS via dashboards pulling from modules like workflow management (audits/collections) and taxpayer accounting (compliance). Automate point calculation with rules engines, triggering real-time updates for managers. Hierarchical roll-up uses organizational trees in user management modules, summing scores bottom-up quarterly.1

Customization draws from existing services: risk analytics for compliance risks, reporting for trends. Security via role-based access ensures only aggregates are visible upward, preserving privacy. Annual reviews link scores to incentives, using ITAS audit logs for verification.31

New Zealand’s Inland Revenue Framework

New Zealand’s Inland Revenue (IRD) employs a Performance Measurement Framework tracking service delivery against government targets via IT systems. It monitors outputs like compliance yields and taxpayer satisfaction, using ranges tied to appropriations (e.g., 85% requests finalized in 28 days). Scores aggregate from frontline processing to executive oversight, with historical data calibrating realistic bands.61011

IRD’s business transformation integrates ITAS-like systems for real-time metrics on voluntary compliance and debt management. This resulted in sustained high performance, with frameworks evolving to balance ambition and achievability.12136

UK’s HMRC Compliance Focus

HM Revenue & Customs (HMRC) uses lead measures like tax gap (5.3% in 2023-24) and compliance yield (£15bn year-to-date). KPIs break into cash yields, revenue prevented losses, and fraud prosecutions (91% court success), with quarterly ranges against annual targets. IT systems enable granular tracking, rolling up to close gaps systematically.7

Ranges are calibrated via multi-year trends, ensuring ~20-30% top performance while addressing fraud (127 prosecutions). This points-based aggregation drives organizational accountability.7

Australia’s ATO Regulator Metrics

The Australian Taxation Office (ATO) aligns with Regulator Performance Framework KPIs, measuring efficiency via service commitments (85% in 28 days). Metrics cover stakeholder engagement, timeliness, and risk focus, using ITAS data for evidence. Ranges prevent undue impediments, with narratives explaining variances.11

Aggregation from activity metrics ensures balanced scores, refined by consultations. This supports good regulatory practice without overreach.11

Singapore IRAS Adaptations

Singapore’s Inland Revenue Authority (IRAS) incorporates performance cycles with rating scales (e.g., 1-5 levels) compliant with employment laws. KPIs include quota attainment analogs for compliance, with objective criteria for remote evaluations. IT integration automates scoring from filing/payment data.14

Ranges emphasize fairness, with appeals processes, achieving high voluntary compliance.14

Canada CRA Challenges and Lessons

Canada Revenue Agency (CRA) faced issues in performance gauging, with inconsistent rule application and poor metrics for relief/audits. Auditor reports highlighted needs for better ITAS-linked ranges to ensure equity, especially for large taxpayers. Reforms emphasize accurate reporting via standardized bands.15

European Experiences: Germany and France

Germany’s Finanzverwaltung tracks administrative costs against revenues, with surveys showing >20% ratios prompting efficiency ranges. France’s DGFiP uses indicators for compliance and service, integrated in IT systems. Both calibrate via historical data for realistic hierarchies.1648

Asian and African Insights

India’s Income Tax Department leverages GSTN for metrics like return processing, with points systems. South Africa’s SARS framework emphasizes compliance yields, calibrated against gaps.58

Global Lessons and Best Practices

Worldwide, TADAT’s nine Performance Outcome Areas (e.g., risk management, voluntary compliance) rate A-D, informing range designs. Balanced Scorecard adaptations link OECD indicators to scores. IMF notes high-performing administrations close gaps via ITAS metrics.425

Success factors: data-driven calibration, ITAS automation, hierarchical aggregation. Challenges like Canada’s underscore fair ranges. Adopting these yields sustainable improvements.9815

Written with the support of perplexity.ai.

-

Understanding an Integrated Tax Administration IT System (ITAS) ↩︎ ↩︎ ↩︎ ↩︎ ↩︎

-

TADAT: Assessing the Performance of Tax Administrations - Blyce ↩︎ ↩︎ ↩︎ ↩︎ ↩︎ ↩︎

-

Defining success: what KPIs are driving the Tax function today? - PwC ↩︎ ↩︎

-

Closing the Gap: How Tax Administration Performance Shapes Compliance ↩︎ ↩︎ ↩︎ ↩︎

-

Our performance (2024) - Inland Revenue (New Zealand) ↩︎ ↩︎ ↩︎

-

HMRC performance data 2025 to 2026: October - GOV.UK ↩︎ ↩︎ ↩︎

-

Core Information Technology Systems in Tax Administrations ↩︎ ↩︎

-

Australian Taxation Office - Regulator Performance Framework Metrics ↩︎ ↩︎ ↩︎

-

The power of data in digital transformation: Inland Revenue New Zealand shares its experience ↩︎

-

Germany’s Tax Revenue and its Total Administrative Cost - HAL ↩︎